Compare Traditional Medicare and Medicare Advantage

Traditional Medicare Plans in Detail

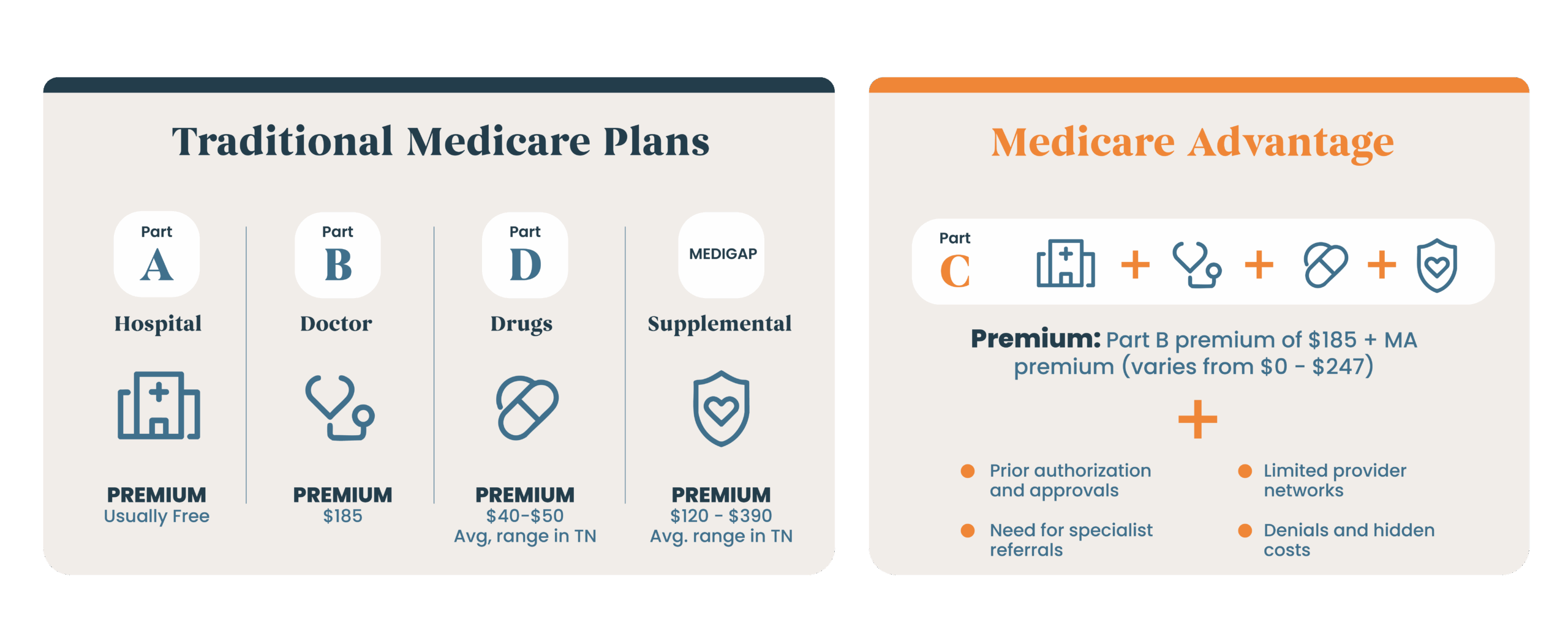

Traditional — Part A

Covers hospital care

Covers 80% of the cost for most medical bills

Can use any hospital that takes Medicare, anywhere in the U.S

Can add on additional coverage o help with unexpected costs

Can add drug coverage

Premium: Usually Free

Traditional — Part B

Covers doctor’s care

Covers 80% of the cost for most medical bills

Can use any doctor that takes Medicare, anywhere in the U.S

Can add on additional coverage o help with unexpected costs

Can add drug coverage

Premium: $185

Traditional — Part D

Optional plan that adds drug coverage to Traditional Medicare

Premium: Average range in TN is $40-50

Traditional — MediGap

Supplemental optional plan that helps pay your out-of-pocket costs that Part A and B don’t cover – like your 20% coinsurance

Your benefits won’t change, and as long as you pay premiums you keep your coverage

Premium: Average range in TN is $120 – $390

Medicare Advantage in Detail

Medicare Advantage — Part C

Bundles hospital care, doctor’s office care, supplemental coverage and drug coverage into one plan

Benefits are provided by a commercial insurance company

You are restricted to using only the doctors and hospitals in your plan’s network

You may need to get approval (prior authorization) from your plan before it covers certain types of care

Plans may offer some extra benefits that Traditional Medicare doesn’t

May not cover your care if you are away from your hometown area

Premium: Part B premium of $185 + MA premium (varies from $0 – $247)

Medicare Advantage Hidden Costs

Out-of-Network Charges If you see a doctor or go to a hospital outside your plan’s network (except in emergencies), you may pay much more—or even the full cost—for care.

Prior Authorization Delays or Denials Prior authorizations can lead to delays in care or denied coverage, shifting unexpected costs back to you.

Higher Out-of-Pocket Costs for Complex Care Medicare Advantage plans often have copays and coinsurance for each service which can add up quickly if you have an illness, injury, or chronic condition.

Missed Medigap Opportunity If you later switch from Medicare Advantage to Traditional Medicare, you may not be able to buy a Medigap plan—or it could cost more—due to medical underwriting.

Limited Access to Specialized Care Some top specialists, hospitals, or academic medical centers may not accept Medicare Advantage plans, meaning you’d pay full price for out-of-network care or be forced to switch doctors.

Annual Changes to Coverage Benefits, provider networks, and out-of-pocket costs can change every year, requiring you to carefully review your plan annually to avoid surprises.

Medicare Advantage plans may seem like a simpler, lower-cost alternative to Traditional Medicare. However, simplicity and lower monthly premiums typically come with tradeoffs:

Tedious prior authorization processes

Need for specialist referrals

Limited provider networks

Higher overall costs due to care denials and hidden costs.

The Bottom Line

Traditional Medicare + Medigap is best if you:

Want more predictable healthcare costs.

Prefer the freedom to get care from the doctors and hospitals you want.

Prefer to pay more in monthly premiums in order to avoid commercial health insurance red tape that can cause care delays and denials.

Medicare Advantage is best if you:

Want to save on monthly premiums and are prepared to pay more out-of-pocket if serious health issues arise.

Prefer to have all of your healthcare coverage bundled into one plan and want “bonus” benefits like a gym membership or wellness program.

Are comfortable with limited provider networks and the need for prior approvals and referrals for most services.